توضیحات

چکیده

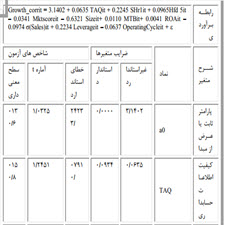

به رغم اینکه طی سال های اخیر در این کشورهای رشد بازارهای سرمایه و جذب سرمایه از طریق سرمایه گذاری ها افزایش یافته است ولی سهم آن در قیاس با تامین مالی از طریق تسهیلات بانکی ناچیز است. دلیل این امر آن است که بازار سرمایه از کارآیی لازم برخوردار نبوده و اطلاعات مربوط به قیمت و مبادلات سهام و اطلاعات پایه ای که بسیاری از شرکت های بزرگ دولتی را در فهرست شرکت های سودآور و کارآمد قرار داده، درست نیست. به همیین جهت رشد بازارهای سرمایه نتوانسته است محدودیت های مالی در شرکت را مرتفع و تخصیص منابع کارآمد سرمایه ای را در این کشورها در پی داشته باشد که این امر ممکن است به سرمایه گذاری کمتر از حد نیاز منجر شده باشد. هدف از این پژوهش، تعیین ارتباط بین کیفیت اطلاعات حسابداری وگزینه سرمایه گذاری درشرکت های پذیرفته شده دربر اوراق بهادار تهران می باشد. با توجه به برقراری همه پیش فرضها از رگرسیون خطی چندگانه مبتنی بر تحلییل داده های تابلویی با اثرات تصادفی ارتباط بین متغیرها برآورد شده، نتایج تحقیق نشاد داد که بین کیفیت اطلاعات حسابداری در ابعاد کیفیت اقلام تعهدی، پایداری سود، هموارسازی سود و قابلیت پیش بینی سود با گزینه سرمایه گذاری رابطه مستقیم وجود دارد.

مقدمه

درسالهای اخیر مطالعات بسیار زیادی در زمینه بررسی ارتباط با کفایت و کارآمدی سرمایه گذاری، اوامل موثر بر آن ویژگی های شرکت ها انجام شده است. به اعنوان مثال، میتوان به مطالعات افرادی مانند کیلان و همکاران (1997) هوبارد (1998) ونگ و همکاران (2009) پاولین و رنه بوگ (2005) ریچاردسود (2006) ودر ایران محمودآبادی و رحایی(1393) محمودآبادی و مهتری (1390) مدرس و حصارزاده(1387)و مشایخی و محمدپور(1393) اشاره کرد.در همه این تحقیقات به رغم تکیه بر مفاهیم مالی سرمایه گذاری در قالب پروژه هایی چود توسعه خط تولید، سرمایه گذاری بلند مدت در سهام دیگر شرکت ها و مواردی از این قبیل و تلقی کارآیی آن در قالب منفی بودن خالص جریاد نقدی پروژه ها، به دلیل محدودیت در دسترسی به اطلاعات داخلی شرکت ها در این رابطه از مفاهیم حسابداری سرمایه گذاری و مخارج سرمایه ای بهره جسته اند. در همه این تحقیقات پرداختن به کفایت و کارآمدی سرمایه گذار و به دست آوردن شواهد تجربی در این زمینه را ضرورتی انکار ناپذیر تلقی نموده اند مشایخی و محمدپور، 1393.)

ABSTRACT

In spite of the fact that in recent years in these countries growth of capital markets and raising capital through investment has increased, its share is negligible compared to financing by banking facilities. The reason for this is that the capital market is not as efficient as possible, and it is not true that information on prices and stock exchanges and the basic information that many large state-owned companies put on the list of profitable and efficient companies. In the same vein, the growth of capital markets has not been able to outweigh the financial constraints on the company and result in the allocation of efficient capital resources in these countries, which may lead to less investment than needed. The purpose of this research is to determine the relationship between the quality of accounting information and the investment option in accepted companies in Tehran Securities. Given the establishment of all assumptions, multiple linear regressions based on analyzing panel data with random effects of the relationship between estimated variables, the results of the research did not conclude that the quality of accounting information in terms of the quality of accruals, profitability, profit smoothing and predictability There is a direct relationship to the investment option.

INTRODUCTION

In recent years, many studies have been done to examine the relationship between the adequacy and efficiency of investment, and the effective impact on those characteristics of companies. For example, studies of people like Kilian et al. (1997) Hubbard (1998) Wang et al. (2009) Pavlin and Rene Boog (2005) Richardsworth (2006) and in Iran Mahmoud Abadi and Rahhani (1393) Mahmoud Abadi and Mehtahi (2011) Modarres and Hesarzadeh (2008), Mashayekhi and Mohammadpour (1393). In all of these investigations, despite the reliance on investment finance concepts in the form of projects for the development of the production line, long-term investment in other companies’ shares and some of these Such as and considering its effectiveness in terms of the net negative cash flow of projects, due to the limited access to internal information of companies in this regard, the concepts of capital account Ray and capital expenditure have benefited. In all these investigations, paying attention to the efficiency and efficiency of the investor and obtaining empirical evidence in this regard is considered indispensable. Mashayekhi and Mohammadpour, 1393.)

Year: 2018

Publisher : First National Conference on Accounting and Management

By : Inspired by Inspiration, Dr. Mohagheghi

File Information: Persian Language/ 11 Page / size: 414 KB

Only site members can download free of charge after registering and adding to the cart

سال : 1397

ناشر : اولین همایش ملی حسابداری و مدیریت

کاری از : الهام خطیری ، دکتر محققی

اطلاعات فایل : زبان فارسی / 11 صفحه / حجم : KB 414

نقد و بررسیها

هنوز بررسیای ثبت نشده است.